The demand for greater profitability as well as the increase in audit frequency have led companies to need more refined and robust cost and budget management. The challenge is to be able to control, analyze, report, and anticipate costs more precisely. This requires specialized cost managers who have the experience and rigor to do so.

Today a company is constrained in how to record and report their financial transactions by various governing bodies. Guidance is provided by organizations, such as the International Accounting Standards Board (IASB), who provide standard principles such as the International Financial Report Standards (IFRS). Then there are also tax laws in each country.

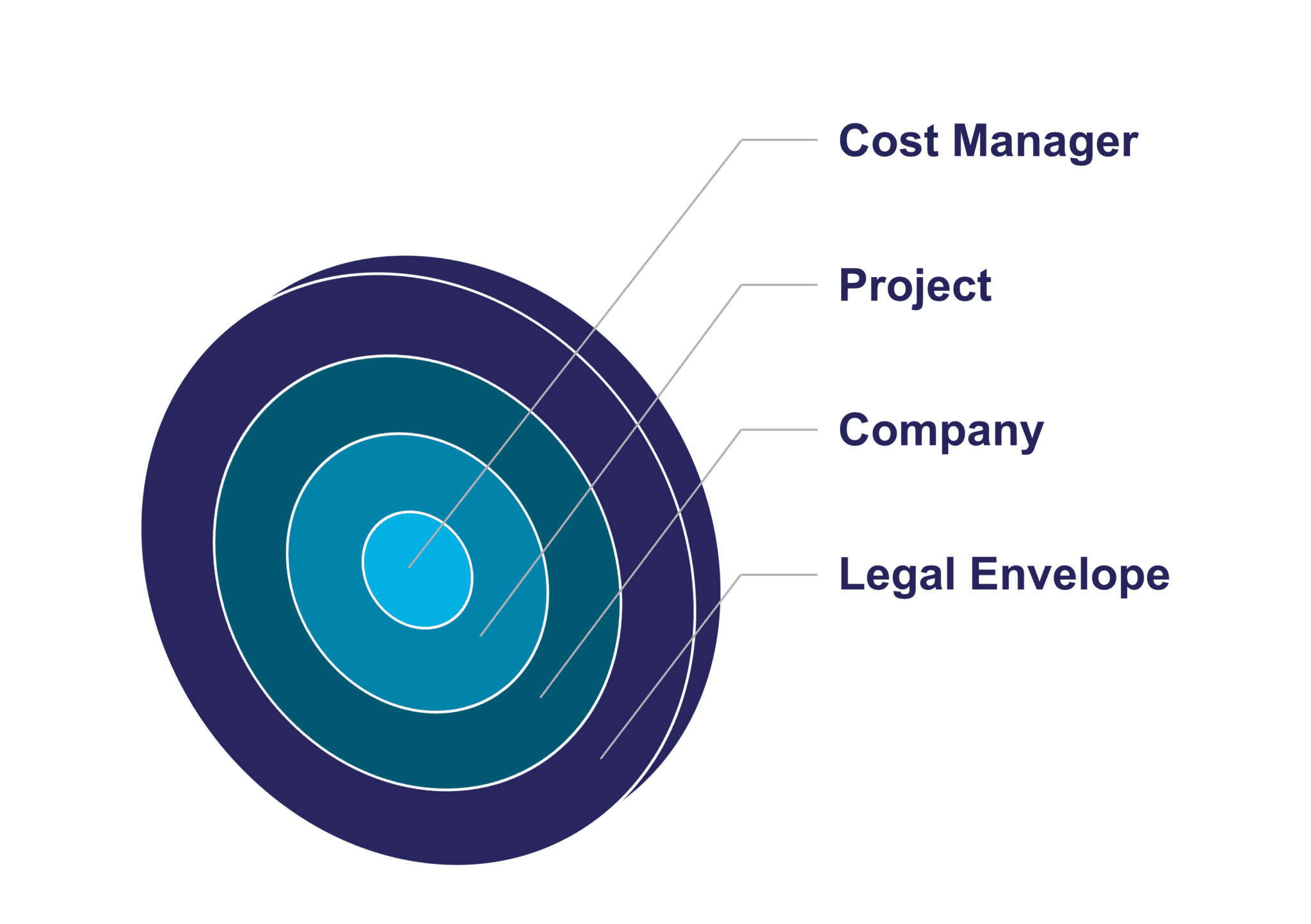

This whole legal envelope is first applied to the company, whose finance staff takes it into account for regulatory reporting, tax filing, and management reporting. They put in place rules and procedures to ensure their organization follows all legal requirements. These rules and procedures are passed on to the project to be managed by the cost manager.

As long as the company remains within this framework, it can adjust its cost management plan as the law leaves room for it. A company can also manage its costs very globally or in a more detailed way. Either way, the cost manager must be financially accountable because the project (and therefore the company) must be held to account. It’s all about being answerable to the above entity, whether they are local, national, multinational, or global.

Consider the following financial and reporting obligations:

Depending on the type of accounting they choose (cash basis or accrual basis), companies can decide when their fiscal reporting year starts and stops based on what best captures their financial cycle. This enables them to fulfill their financial and reporting obligations.

A company’s accounting requirements must be considered in their project cost management strategy. Additionally, there are 4 types of project costs:

There are different types of costs, which often complement each other:

We can also distinguish the different costs by their nature within a project, which is more granular than those described above. Here are some examples of different costs that can be found in a project:

Understanding these different types of cost as well as the legal accounting requirements makes it possible to define the methods used in managing a project. This allows us to budget, analyze, plan, and control the project costs.

In our next article, we will look at the four phases of cost management.

This article series was written by Aurélien CRÔNIER and Mehdi DARD with contributions from Fanny DA SILVA and the MIGSO-PCUBED Cost Management Community of Practice.

[1] Source: The Standish Group