Guide

Cost management is an activity we are confronted with daily. Shopping, buying a car, or preparing for a vacation are all activities that beg the question: What is my budget, and how much can I spend? This question also arises for any company and any project; the challenge is to respect the defined budget as much as possible.

Keep in mind that on average, one out of every two projects is delivered with a deviation in one of the project Triple Constraints (scope, cost, time).[1] This means that cost, one of these three elements, plays an important role in project success and must be closely managed.

In this guide, we will explain what cost management is and the different types of costs that exist. Written by our very own consultants who work on global industrial projects, we hope this article helps you to apply these concepts in your own projects.

Project Cost Management is the process of assessing, monitoring, and controlling the costs of a project, in line with both the project budget and the organization’s financial requirements. It is also one of the core functions of Project Controls, a typical part of PMO operations, along with schedule management and risk management. The scope of cost management is vast, including the control, analysis, or even forecasting of a given budget.

As project cost management is so connected to the budget, you may wonder what is the difference between cost and budget management? Budget management is more related to the management of the company, whereas cost management is more project-focused. Nevertheless, project cost managers naturally have budgetary responsibilities. After all, following the budget is one of their primary objectives in keeping projects on track.

Cost management has been around since the dawn of project management itself, especially when project success is often determined by its financial outcomes. However, cost management has long been managed internally and rarely outsourced to external contractors. A lack of companies’ in-house expertise in this area, a greater diversity of cost types, as well as the advancement of project management methodologies have paved the way for a more developed financial mindset.

As companies’ focus has expanded around reducing costs and increasing profitability, this pressure is increasingly reflected in projects, putting proper cost management at the forefront. Today, therefore, we see a greater need for specialized cost managers on project teams.

The primary objectives for effective cost management are:

The demand for greater profitability as well as the increase in audit frequency have led companies to need more refined and robust cost and budget management. The challenge is to be able to control, analyze, report, and anticipate costs more precisely. This requires specialized cost managers who have the experience and rigor to do so.

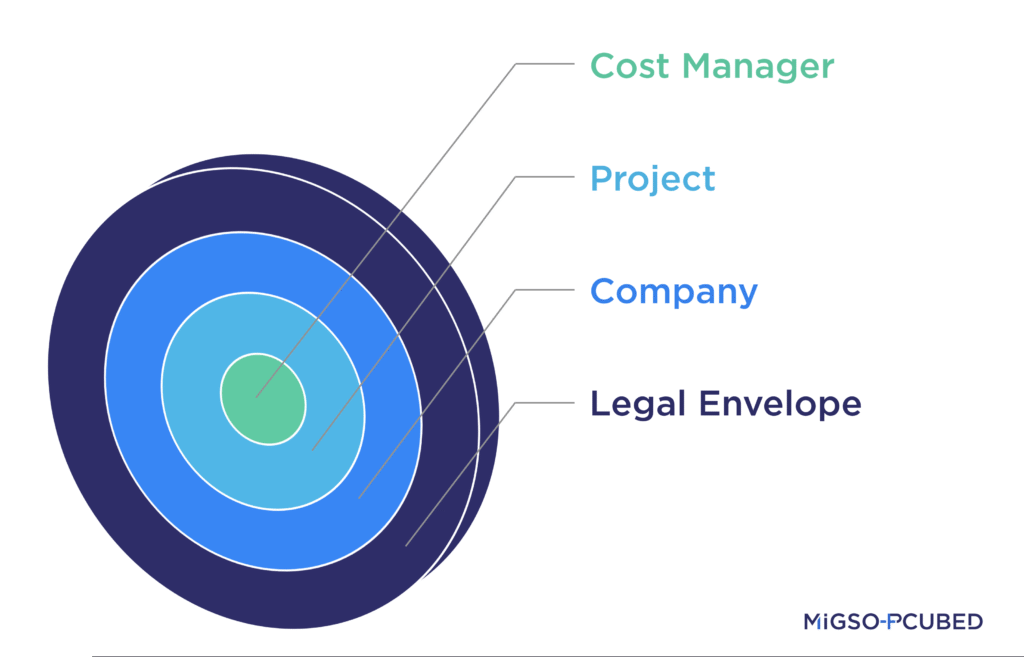

Today a company is constrained in how to record and report their financial transactions by various governing bodies. Guidance is provided by organizations, such as the International Accounting Standards Board (IASB), who provide standard principles such as the International Financial Report Standards (IFRS). Then there are also tax laws in each country.

This whole legal envelope is first applied to the company, whose finance staff takes it into account for regulatory reporting, tax filing, and management reporting. They put in place rules and procedures to ensure their organization follows all legal requirements. These rules and procedures are passed on to the project to be managed by the cost manager.

If the company remains within this framework, it can adjust its cost management plan as the law leaves room for it. A company can also manage its costs very globally or in a more detailed way. Either way, the cost manager must be financially accountable because the project (and therefore the company) must be held to account. It’s all about being answerable to the above entity, whether they are local, national, multinational, or global.

Consider the following financial and reporting obligations:

A company’s accounting requirements must be considered in their project cost management strategy. Additionally, there are 4 types of project costs:

There are different types of costs, which often complement each other:

We can also distinguish the different costs by their nature within a project, which is more granular than those described above. Here are some examples of different costs that can be found in a project:

Understanding these different types of cost as well as the legal accounting requirements makes it possible to define the methods used in managing a project. This allows us to budget, analyze, plan, and control the project costs.

In order to establish a cost management framework for your projects, it is necessary to understand the different phases of the cost management process; from defining a cost management plan to delivering your reports. Learn the four key steps of this process.

One of the challenges in managing your project’s costs well is understanding your company’s environment, including its different stakeholders. This often falls on the shoulders of the cost manager, the central liaison between project, finance, and management teams.

Earned Value Management is a method that allows us to correlate a project’s schedule with its cost in order to determine if the project is performing well or not. Discover how to calculate and interpret Earned Value.

Thank you to Aurélien CRÔNIER, Mehdi DARD, Fanny DA SILVA, and the MIGSO-PCUBED Cost Management Community of Practice for contributing to this article.

[1] Source: The Standish Group

Choose your language

A quarterly digest of our best articles on all things Project Management.

Subscribe to our

Newsletter!

Our website is not supported on this browser

The browser you are using (Internet Explorer) cannot display our content.

Please come back on a more recent browser to have the best experience possible