In order to define project risk management, we first need to define project related risks and opportunities. Risk and opportunity are described by at least 3 basic characteristics: an event, a probability of occurrence and potential impacts on the project objectives. These must be self-explanatory and can be supplemented by its causes.

“A project risk is an uncertain event that, if it occurs, has a negative impact on at least one of the project’s objectives (Time, Cost, Quality, Scope, Performance).”

For example, a risk event could be: “the inability of supplier X to conduct feasibility studies on a modification Y by the end of 2025’ “. The causes of this risk could be due to the supplier’s resources being heavily utilized on other projects and the impacts of the COVID-19 crisis. The consequences would be a delay in implementing change Y. A risk response strategy could be to subcontract out the work or to identify other internal resources capable of conducting the study.

An opportunity, on the other hand, is an uncertain event that, if it occurs, has a positive impact on at least one of the project’s objectives. For example, an opportunity could be: “Do not perform activity Z”.

The causes of the opportunity could be due to some feasibility studies in progress, and the consequences would be a financial gain equal to the cost of activity Z. The possible response strategy allowing this opportunity to occur could be to bypass activity Z, leading to a decision not to carry out activity Z (partially or totally).

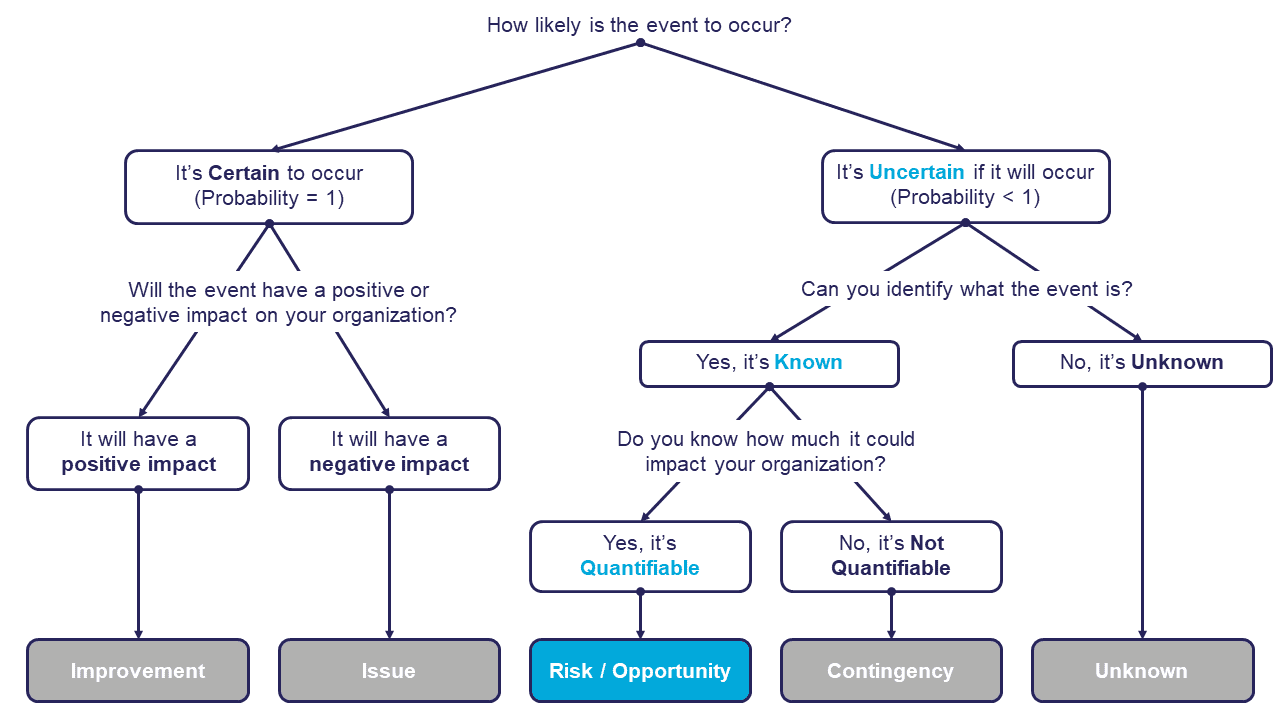

It is common to confuse the notion of unknown, contingency, risk, issue, and improvement. A clear distinction must be made to ensure effective risk management. See breakdown in Figure 1 below.

Although they are outside the scope of risk management, unknowns should not be underestimated. They can significantly impact the project objectives (time, cost, quality).

Risk management involves anticipation. Its objective is to guide companies in preparing for, reducing, or avoiding the negative impacts created by any known event. It also helps to improve opportunities with positive repercussions.

Why start now?

The COVID-19 pandemic has had various impacts around the world, some of which we would never have expected. In the professional world, each company has been affected differently and not all have reacted in the same way. Some were unable to produce because raw materials could not be delivered to them, while their competitors had enough stock to compensate for delivery delays. Some lacked cash flow to survive for an extended time, while others had enough savings to get them through the difficult period.

In these situations, we have been able to more clearly distinguish those companies that were already paying close attention to risk management before the health crisis. It is in the face of new difficulties that, knowingly or not, we will try to better anticipate or predict the unpredictable and to protect ourselves against uncertainties of all types. The trick now is to do it with the level of structure required by your company, department, or project.

At MIGSO-PCUBED, our experience has shown that risk and opportunity management is essential to success. This begins with developing an organizational risk management strategy. Then the organization can define their risk management process and engage a team of experts to manage it.

A sound risk management strategy helps you to look to the future, capture opportunities that come your way, and deploy the right efforts against any threats.

In our next article, we will review the 5 Key Elements for Implementing Project Risk Management into your organization.

This article was written by: Marie BELGODERE, Jérémie CLAUSTRE, Capucine COMTE, Alioune DIALLO, Emmanuel LATGE, Jessy MIGNOT, Ingrid NGOBAY, Pierre PETILLON, Louann SUGDEN, Chris WAMAL.